iHeart Media‘s purchase of design podcast 99% Invisible means that the canary in the coalmine just died.

In the past couple of years, two high-profile acquisitions of podcast companies have produced a whirlwind of think pieces from the media press. Forbes (12/4/20) prophesied that Amazon’s 2020 purchase of podcast publisher Wondery put the industry “on a Path to a Crossroads.” And a Poynter headline (2/7/19) proclaimed Spotify’s 2019 purchase of celebrated commercial podcast network Gimlet Media “could change podcasting’s future.”

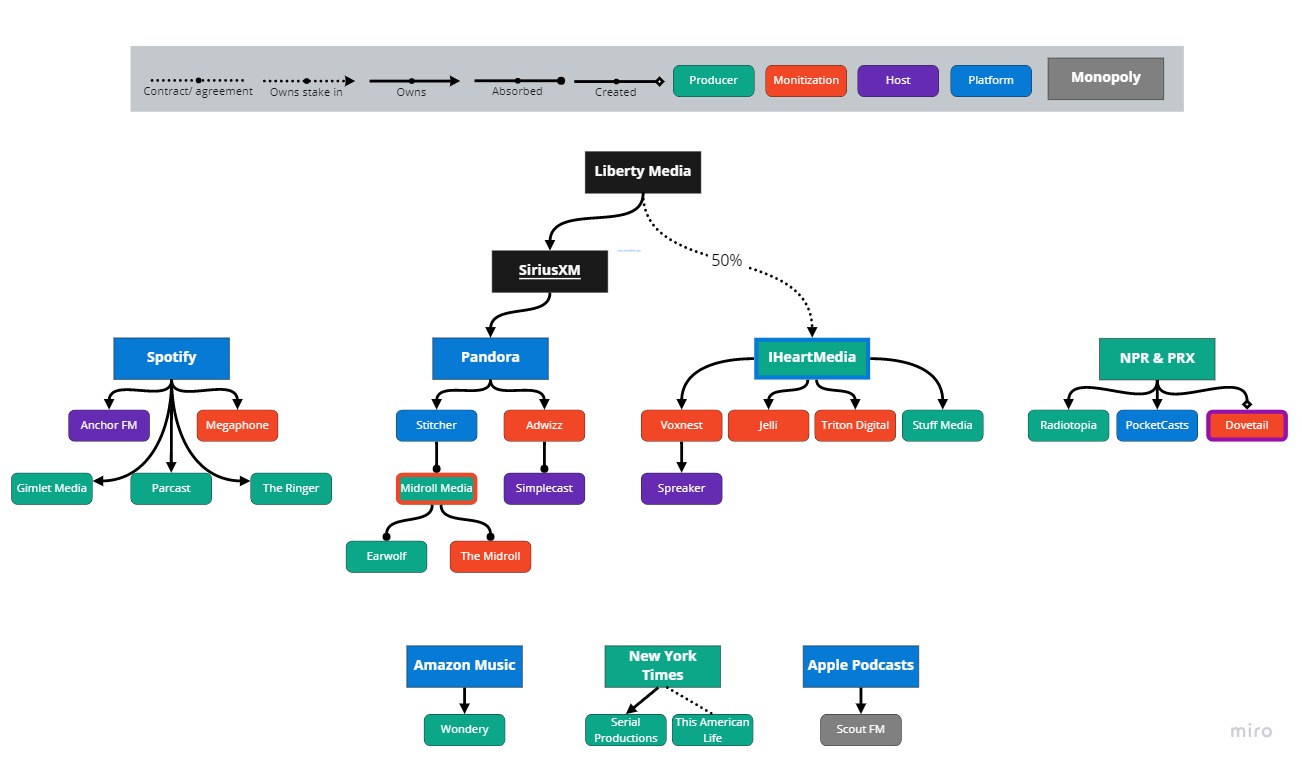

But that future has already arrived. In a largely ignored story last year, Liberty Media, a conglomerate that already owns SiriusXM radio and the audio streaming and podcast platform Pandora, secured the right to a 50% stake in radio and podcast producer iHeartMedia (formerly Clear Channel). It currently holds 40%.

That left the podcast industry dominated by a handful of players—with Liberty, Spotify and public radio (via NPR and PRX) in the drivers seat, and Amazon, Apple and the New York Times not far behind. The new podcast oligopoly has arrived, and monopoly is on the horizon.

In April, the final “canary in the coalmine” of industry consolidation keeled over dead: iHeartMedia bought 99% Invisible, the vaunted architecture and design podcast often held as a standard bearer of the noncommercial podcasting space.

This is a far cry from podcasting’s past, which featured an ecosystem of independent companies that separately produced, hosted, distributed, platformed and monetized content. The medium’s advertising market is 20% the size of radio, but it’s projected to top $1 billion in ad revenue this year and continue to grow. Large media corporations realized if they consolidated these services and combined them with targeted advertising, podcasting could become a veritable “money spout” for whoever captured a large swath of listeners.

The Spotify empire

Spotify may be best positioned to open that money spout. It’s arguably the most popular podcasting platform in the US, and the press sometimes compares the company to Netflix because of its sizable investments in content. Over the past two years, Spotify has purchased high-profile producers (often styled “networks”), acquiring Gimlet, The Ringer and Parcast, and signed exclusive licensing deals with Joe Rogan, DC Comics, Kim Kardashian West and Michelle Obama.

Spotify is arguably the most popular podcasting platform in the US.

Producers and platforms have often been the first to merge in the monopolistic “podcast wars,” and typically get media attention as the most visible pieces of the industry. But as a Verge headline (2/17/21) argues, “The Podcast Wars Will Come Down to Ad Tech, Not Exclusive Content,” and if that’s true, Spotify‘s purchase of Anchor FM and Megaphone (formerly Slate’s Panopoly) are much more important.

Megaphone is a podcast monetization company that makes money for producers by inserting ads into their content. Anchor is a podcast hosting company that stores the audio, distributes it to the various platforms, and gathers analytics about numbers and demographics of listeners.

Anchor’s “one-stop shop” technology allows publishers to record, host, distribute and even monetize their content. The ease with which it allows amateurs to start a podcast quickly made the company one of the most popular hosts on the market. Spotify has used its purchase of Anchor to lower the barrier to entry even more, adding 1 million new shows on the platform in 2020 (Verge, 12/2/20). That brings in more listeners and potential subscription revenue, and means more ad inventory the company can sell.

Anchor’s ad tech has struggled to make money for amateur publishers, but with the help of advertising-focused Megaphone, Spotify launched its “final infinity stone” last month: a full-on automated advertising suite (Input, 2/22/21). Combining a platform (Spotify) with hosting (Anchor) and new dynamic ad-insertion technology (Megaphone) means advertisers can collect audience data and serve “different ads to different listeners” in real time, wrote Ken Doctor in Nieman Lab (1/13/16). This “could mean a 400% jump in ad capacity” by placing ads on old content as well as new.

This is the coup de grâce of the podcast monopoly wars. More audience analytics means more ad revenue for publishers, which brings more publishers to the platform, which means more listeners, which means more audience analytics, ad infinitum.

Podcast consolidation. (See larger view.)

Monopoly lessons

“If Spotify can leverage cheap capital to lock a large audience into its ecosystem, podcasts would need to go there,” warned YouTube veteran Hank Green (Washington Post, 5/27/20).

If this model reminds you of another large company besides Netflix, you’re not offbase. In the Washington Post (5/27/20), veteran YouTuber Hank Green wrote:

My guess—and I’m hardly alone—is that Spotify wants to become to podcasts what YouTube is for video: simply, the default platform for both listeners and creators. And that should worry people in both of those groups.

In the early- to mid-2000s, this monopolistic system allowed YouTube to foster a vibrant community of DIY creators through its “Partner Program,” which enabled many to make a living with dedicated audiences as small as 10,000 subscribers. But those creators soon faced the consequences of enmeshing their livelihoods with Google. which bought YouTube back in 2006.

YouTube‘s ever-changing algorithm has burned out creators and decimated their audiences. The company has threatened to demonetize content—taking away ad revenue—to force its partners to sign contracts beneficial to Google, and changed the terms of the program overnight. Today, the company has largely left its erstwhile indy stars in the lurch as it pursues safer, more sanitized content palatable to its advertisers.

Wrote Green:

In the ecosystem of YouTube, which Google owns, tens of thousands of small businesses depend on the whims of one of the largest companies in the world for both audience and revenue.

Implications for publishers and listeners

We’re seeing a glimpse of what that could look like for publishers on the new podcast uber-platforms. Publishers gain a lot from being owned by one of the new oligopolists, but it comes at a cost. PJ Vogt, a former host of the popular Gimlet podcast Reply All, pointed out on Twitter (11/4/20), “Since Spotify acquired Gimlet, we do not have any say in rejecting advertisers.”

Amazon Music attempted to require podcasts on its platform to “not include advertising or messages that disparage or are directed against Amazon,” before backing down in the face of backlash (Input, 8/12/20).

Ashley Carman in the Verge (11/11/20): “We all might end up having to use Spotify whether we like it or not.”

The biggest changes for listeners will come from targeted advertising. Its absence from podcasting reduced revenue for creators, but meant digital audio was one of the final provinces where people maintained some reasonable expectation of privacy. Megaphone, Anchor and their ilk spelled the end of that, and consolidation has taken it further by concentrating users’ personal information on fewer and fewer platforms. Wrote Ashley Carman for the Verge (11/11/20):

Spotify knows listeners’ names, billing information, where they live, their age, what music they like, the other shows they enjoy, who they’re friends with on Spotify, what devices they use and plenty of other data.

In 2020, Spotify filed a patent for technology that tracks its users’ personality traits, which it could employ to change the tone of voice of advertising on the platform (“upbeat” for extroverts and “soft-toned” for introverts, etc.). And this year, it filed a second patent to identify users’ “emotional state, gender, age or accent” by recording them. The inventors of the first patent wrote in a research paper that their future research “could begin to link streaming behavior with brain scanning, genetic and physiological data” (Music Business Worldwide, 10/7/20, 1/27/21).

Spotify started selling personalized playlists to brands in 2019 (Vox, 1/11/19), and we can expect something similar for podcasts coming down the pipeline. Pandora has also recently come out with a new analytics tool that “will tell podcast hosts where their listeners live and how long they listen,” according to the Verge (6/18/20).

Liberty and future contenders

Liberty Media and its podcasting holdings.

Spotify and Apple Podcasts compete for the most listeners on their platforms, but Liberty is the only true competitor with Spotify for an all-in-one platform, via its audio-streaming platform Pandora. In 2018, Liberty’s satellite radio company SiriusXM bought Pandora for an epic $3.5 billion. Later that year, Liberty bought podcast monetization company Adwizz, followed in 2020 by host Simplecast, and folded them into Pandora to create “a full-on podcast distribution and monetization system” (RAIN News, 6/17/20). Later in 2020, Sirius closed the loop by adding producing, and much, much more, when it bought the already-consolidated producer-platform-monetization company Stitcher from the E.W. Scripps media conglomerate.

Stitcher’s own earlier consolidations are a good case study on how the stage was set for the insta-monopolies formed in the late ’10s. In 2014, monetization company Mid Roll and podcast publisher Earwolf merged into Midroll Media. In 2015, Scripps bought Midroll, followed in 2016 by then-podcast platform Stitcher. In 2018, Scripps merged all these parts together into a single company under the Stitcher brand.

Perhaps wary of Spotify‘s success, and the machinations of Apple and Amazon to create their own podcast walled gardens, Liberty is hedging its bet that Pandora will come out on top. The conglomerate secured the go-ahead from regulators to buy a 50% stake in iHeartMedia last year, and has since increased its share to 40%. A legacy commercial radio broadcaster better known by its former name Clear Channel, iHeart has focused on distributing content to as many platforms as possible rather than pushing users to its own. But it has also held its own in the consolidation wars when it comes to combining all the spokes of the industry.

In 2018, iHeart bought publisher Stuff Media and targeted ad company Jelli. In 2020, it acquired another monetization company called Voxnest, which itself already owned hosting company Spreaker. In February 2021, it tied these together with the purchase of the respected monetization and analytics company Triton Digital from Scripps (that company’s last major digital audio holding).

Medium and small podcasting companies have continued to merge over the past few years. Old-time podcast host Lisbyn just acquired monetization company Glow. Music streaming platform LiveXLive bought mid-sized podcast producer PodcastOne in 2020. And monetization-hosting company Acast bought hosting company Pippa in 2019, and the dual platform-advertising company RadioPublic this year, making it a scrappy competitor for the throne. These and other still independent companies, like host-monitizer Art19, could serve to boost one of the lesser oligopolists to prominence with a well-timed purchase.

Spotify and Pandora’s industry dominance began with platforms buying producers. Last year, the New York Times bought the much-vaunted producer Serial Productions from This American Life, home to the “podcasting’s first breakout hit,” in the words of David Carr (New York Times, 11/23/14). Last year Apple bought Scout FM, an application that creates podcast playlists, and just introduced paid subscriptions to its long-standing podcast app (triggering Spotify to do the same). We can be assured there is more to come.

Alternatives to commercial monopoly

Patreon was founded in 2013 with the goal of creating a donation-based subscription model that has proved popular among podcasters.

So what’s the alternative to commercial monopoly? Luminary is pursuing a pure subscription model, avoiding the problems targeted ads bring by eschewing them altogether. Acast has developed a hybrid approach to paywall content listeners can still access across multiple platforms. In 2013, Patreon launched with a vision for a donation-based subscription model that has become popular with podcasters.

Then, of course, there is public radio. From the outset, the three major public radio corporations in the US have been key players in podcast production, accounting for almost 30% of the total audience of the Podtracs top 20 publishers. Today National Public Radio (NPR) competes with iHeartMedia for the top spot, with the Public Radio Exchange (PRX) coming in fifth and American Public Media (APM) 19th.

While commercial podcasting is racing toward oligopoly, public media are holding the line on an alternative vision with a parallel universe of services that reflect the medium’s multi-platform roots. In some ways, this makes public radio odd bedfellows with iHeartMedia, which is pursuing a similar content-focused multi-platform ecosystem. It remains to be seen how Liberty’s purchase of the company may change that formulation.

PRX’s Radiotopia is a bold experiment in organizing and funding a podcast network that blends pieces from the commercial and public podcasting world. Each show in the “federation” shares advertising, distribution, cross-promotion, foundation support and donations, but remains editorially independent.

Radiotopia relies on PRX‘s in-house hosting, monetization and analytics platform Dovetail to dynamically place ads across all of its content. It’s a direct competitor to the likes of Megaphone, Anchor and Adwizz, and can boast of serving ads on Serial, the “fastest-growing podcast of all time” (Medium, 5/18/16).

In what the Verge (3/2/20) called public media’s “answer” to Spotify, NPR and some of its member stations acquired podcast platform PocketCasts in 2018, and the BBC joined the partnership this year. PRX and a number of commercial investors spun off their own platform in 2016, called RadioPublic, though they have since sold it to Acast.

This growing open ecosystem to produce, distribute and monetize podcasts could be dubbed the “PRX model,” a new twist on the oft-celebrated and oft-maligned motley model that has funded public radio in the US for decades through listener donations, foundation support and “underwriting” (i.e., advertising). The dynamism of US public audio funding models is admirable, but they are not without baggage.

Donation-funded media incentivizes content directed towards middle- and upper-class audiences who can afford to donate. The continued reliance on foundations plays into the interests of the nonprofit/industrial complex. And the shift away from regulated radio has loosened public media’s already weak resolve to maintain clear boundaries between their content and advertisements. (In 2016, the head of podcast ad sales for NPR, Bryan Moffett, euphemistically expressed this as taking “advantage of the uniqueness” of podcasting.) Not to mention public media have not been above their own consolidation: Public Radio International merged with PRX in 2018.

Future landscape

Where does this leave us? On the one hand, the new emerging walled garden models of Spotify, Pandora and Amazon can create space for DIY audio producers to thrive, but it puts them at the mercy of monopolist overlords. On the other hand, the open source podcasting world championed by US public media continue to produce some of the most important audio storytelling today, but act as de facto gatekeepers.

One simple answer to this conundrum is true public funding of podcasting and media at large, as with John Nichols and Robert McChesney’s proposal for a $200 tax credit Americans could use to donate to media of their choice. But absent a large-scale movement for media democratization, this is nothing to hold our breath for.

US public radio could band together and expand on their vision with PocketCasts to create a complete competitor to the likes of Pandora and Spotify. But that would represent a full-on pivot from their current strategy, and US public radio as it stands, with its heavy dependence on corporate and foundation money, is far from a perfect steward of a potential public podcast monopoly.

Time will tell how the landscape continues to harden. We will not be waiting for long.

This content originally appeared on FAIR and was authored by Fairness & Accuracy In Reporting.

Fairness & Accuracy In Reporting | Radio Free (2021-05-21T18:48:35+00:00) The New Podcast Oligopoly. Retrieved from https://www.radiofree.org/2021/05/21/the-new-podcast-oligopoly/

Please log in to upload a file.

There are no updates yet.

Click the Upload button above to add an update.